1. Summary

- Over the last 5 years, Dillard’s stock price has increased from $74.57 to $340, a massive 355% increase.

- Despite the revenue spike of 49% and 5.7% in FY 2021 and 2022, respectively, Dillard’s revenue has grown at a weak CAGR of 0.36% over the last ten years.

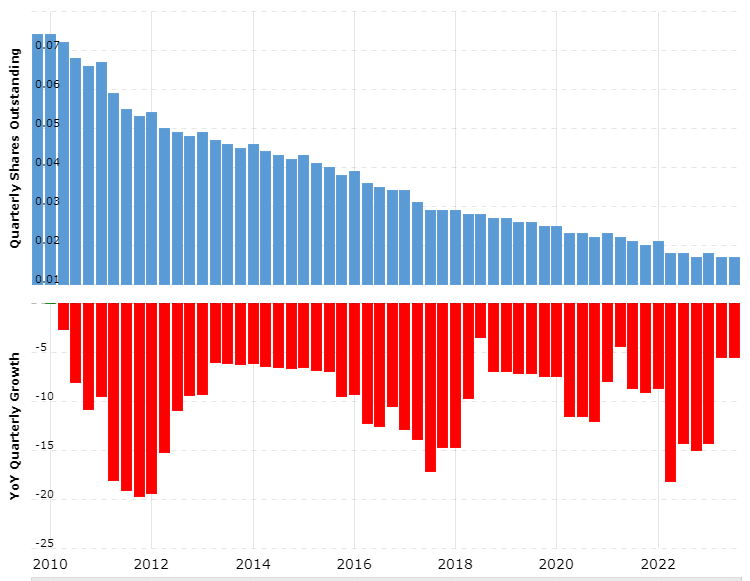

- Although, Dillard’s has reduced its shares outstanding by 77% since 2010, and they are planning to continue on this shareholder-friendly path.

- With the continued decreasing sales and compressing margins experienced during the first quarters of FY 2023, Dillard’s future performance will likely be hit and forced to return to its pre-pandemic levels as the spike in aggregate demand experienced in 2021 and 2022 is vanishing gradually.

2. Dillard’s Stock Performance

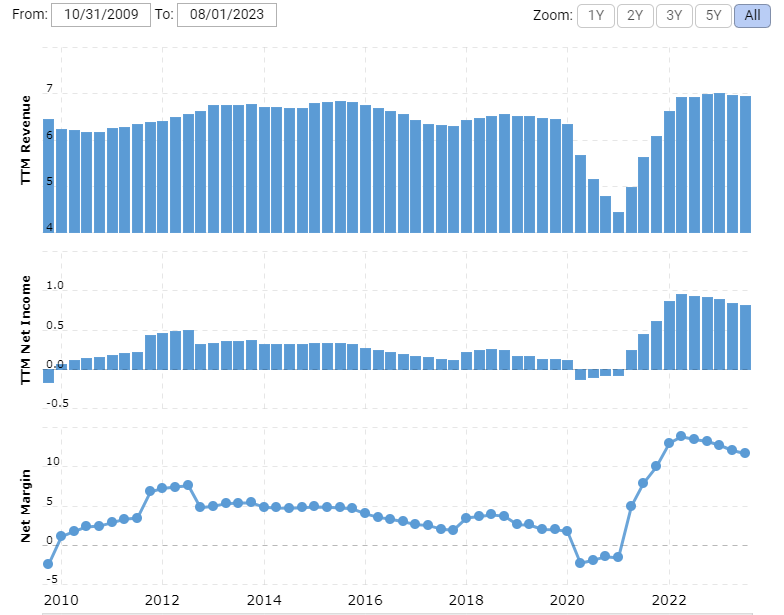

Over the last five years, Dillard’s stock price has increased from $74.57 to $339, an interesting 355% increase. What is more interesting is that since the stock sell off in 2020, the stock has risen by a jaw-dropping 1,123%. Dillard’s sales had a massive boost from the aggregate demand from the COVID pandemic in 2021 when the company’s net income increased 677% to $863 million compared to the $111 million generated in 2019. For FY 2020, Dillard’s Inc. reported net income losses of $72 million. On the other hand, free cash flow increased 349% to $1,176 million in 2021 compared to the $262 million generated in Fiscal Year 2019.

There are a few things that we’re going to highlight in this stock analysis for Dillard’s, Inc. The first thing is to understand what factors drove such a massive increase in the stock price and the financial performance achieved. The second thing we will analyze is the overall history and growth of the company to determine if it has more room for improvement and overperformance compared to its peers. Finally, we are going to determine the underlying value of the company and its prospects, as Dillard’s stock is currently trading at $360 per share, which gives it an attractive p/e ratio of 7.5.

3. Dillard’s Business Overview

Dillard’s Inc. is a relatively family-controlled company founded in 1938 and is one of the nation’s largest fashion apparel, cosmetics, and home furnishing retailers in the United States. The company operates 274 Dillard’s stores, including 27 clearance centers, across 29 states. Dillard’s has a wide selection of premium merchandise from both national and exclusive brand sources offered through its retail operations segment across different sections such as cosmetics, ladies’ apparel, ladies’ accessories and lingerie, juniors’ and children’s apparel, men’s apparel and accessories, shoes, and home and furniture. Dillard’s also operates a general contracting and construction company, and a portion of this contracting business segment includes the construction and remodeling of Dillard’s stores.

Stores

Over the last 10 years, Dillard’s stores have decreased slightly, from 302 stores in 2012 to 274 stores as of Dillard’s Q2 earnings report. They have been remodeling the stores and relocating them to more profitable locations. The total square footage has decreased from 49.2 million square feet in 2016 to 46.9 million square feet in 2023. What is interesting about Dillard’s stores is that they own approximately 92% of their square footage unencumbered, which boosts Dillard’s financial strength as it can lower its operating expenses over the long term

Operating Segments

Dillard’s reports its earnings in two segments: the retail segment and the construction segment. The retail operations segment constitutes 98% of the company’s sales, and the construction segment represents 2%. The cosmetics, ladies’ apparel, ladies’ accessories, lingerie, men’s apparel and accessories, and shoes sections represented 15%, 21%, 14%, 20%, and 15% of the net sales for FY 2022, respectively. while junior’s apparel and home and furniture represented 9% and 4% of the net sales for the same period, respectively.

Besides the retail segment and the construction segment, Dillard’s also perceives revenue through a credit card alliance with Wells Fargo Bank. This alliance gives Wells Fargo the rights to own and manage the private label card accounts for Dillard’s customers, as well as retain the benefits and risks associated with the ownership of the accounts. They also take care of all the processes related to Dillard’s credit cards and its services for customers. This allows Dillard’s to receive ongoing cash compensation from Wells Fargo based upon the alliance portfolio earnings without being responsible for the bad debts and finance charges associated.

Dillard’s Shareholder Structure

As of March 23, 2023, there were a total of 13,013,694 shares of the Company’s Class A Common Stock and 3,986,233 shares of the Company’s Class B Common Stock outstanding.

Class A and B Voting rights: holders of Class A common stock are empowered as a class to elect one-third of the directors serving on the company’s board of directors, and holders of Class B common stock are empowered as a class to elect two-thirds of the directors serving on the company’s board of directors.

Family ownership: Members of the Dillard’s family (the family who founded Dillard’s) own 99% of Dillard’s Class B common stock through W.D. Company, Inc., for which William Dillard, II, Chairman and Chief Executive Officer of the Company, Alex Dillard, President of the Company, and Mike Dillard, Executive Vice President of the Company, are officers and directors of W.D. Company, Inc. and own 27.4%, 27.9%, and 26.3%, respectively, of the outstanding voting stock of W.D. Company, Inc. This denotes a sharp skin in the game when it comes to managing Dillard’s, Inc., as the executive officers, mainly directly related to Willard’s founder, own approximately 30% of Dillard’s overall outstanding shares.outstanding shares.

4. Dillard’s Fundamentals Analysis

Revenue/Sales Growth

For Q2 FY 2023, Dillard’s sales declined by 3% to $1.567 billion compared to the $1.589 reported for Q2 FY 2022. This decline was attributed to cautious customer spending in the first weeks of the second quarter, and comparable store sales decreased by 3% as well.

Despite the revenue spike of 49% and 5.7% in FY 2021 and 2022, respectively, Dillard’s revenue has grown at a weak CAGR of 0.36% over the last ten years. If we take away the unusual growth it experienced in 2021, its performance is even weaker. From FY 2014 to FY 2019, the revenue declined by 6.3% from $6.7 million to $6.3 million as Dillard’s struggled with increasing markdowns and discounts to attract customers in a period where the retail industry was experiencing strong pressure from a shift in the consumer behaviour and preferences in regards to e-commerce and discount retailers, which put pressure on the brick-and-mortar retailers who missmanaged their debt or failed to adapt to the new trends, and favoured strong online retailers like Amazon and Walmart.

Free Cash flow

Free cash flow has grown by an 8% CAGR over the last 10 years. In 2021 alone, Dillard’s free cash flow increased by 677% to $1,176 million compared to the $262 million reported in FY 2019. It has had an amazing increase in FCF during the past 2 years, but when considering Dillard’s performance before the COVID pandemic in 2020, there is a noteworthy lack of sustained growth and performance in Dillard’s business economics, which is important to consider when evaluating Dillard’s future ability to generate cash flow once the post-pandemic demand normalizes.

Net Profit Margin

In Q2, Dillard’s net profit margin decreased to 8.4% from the 10.3% reported in Q2 2022. This denotes the impact that the current tightening economy and the pressure on discretionary spending continue to have on the retail industry. Moreover, Dillard’s did not provide an outlook or expectations for FY 2023, but we expect its net profit margin to continue to tighten and return to its 10-year historical average of 4% or even below given the challenges ahead for the retail industry and the pressure from high interest rates.

For FY 2021 and FY 2023, Dillard’s net profit margin surged to 13%, a significant increase compared to the 3% average from FY 2014 to FY 2015. We are excluding the -2% net profit margin for FY 2020 as the net margins for many retailers were crushed due to the COVID pandemic, and it was an unprecedented period that doesn’t reflect precisely the performance of the company over the long term as Dillard’s historical net profit margin is significantly low compared to the net profit margin achieved in the last two years.

Roe and Roic

When it comes to high returns over equity and invested capital, Dillard’s has performed relatively well but not exceptionally well, with a 10-year average ROE and ROIC of 15% and 19%, respectively. Its performance is significantly better than that of Macy’s, one of its competitors in the retail industry, with a 10-year ROE and ROIC of 15% and 9%, respectively.

Liquidity

Dillard’s liquidity is quite exceptional; the company can pay down its total long-term debt of $555 million in almost a year using its 5-year average free cash flow of $538 million. Moreover, Dillard’s has a current ratio of 2.4 and a debt-to-shareholder ratio of 0.34. These metrics reflect a strong financial position that will serve the company well to sustain and ensure the continuity of its operations in economic downturns and times of uncertainty when discretionary spending tends to decrease significantly and the stronger and better-adapted retailers can take market share from the failing ones.

Stock Repurchase

Dillard’s has been consistent and committed to the repurchase of its shares outstanding, which have come down from 74 million in FY 2010 to 16.4 million on July 29, 2023. This represents a massive 77% decrease, which has significantly boosted Dillard’s shareholders’ return. And this is expected to continue as the company has $458 million remaining under the May 2023 share repurchase program; this represents about 7% of Dillard’s market cap of $5.9 billion.

5. Risks and Concerns

Dillard’s sales and margins have contracted continuously over the past five quarters, reflecting weaker consumer demand and a return to the company’s performance before the aggregate demand from the pandemic boosted its results. For Q2 2023, retail sales and comparable sales stores decreased by 3%, and the net income margin fell from 10.3% in Q2 2022 to 8.4% in Q2 2023. And when we consider that the number of sales transactions during FY 2022 decreased by 3% compared to FY 2021 while the average dollar per sales transaction increased by 8%, there are clear signs that the growth for Dillard’s moving forward is going to be weak as they are not taking market share and their previous growth was due to a combination of decreasing markdowns and consumers willing to spend and pay more, which is unlikely to continue as discretionary spending is under strong pressure and Dillard’s sales come solely from the US.

Additionally, Dillard’s actions for navigating these uncertain periods and future growth are not clear; the company has not communicated what its strategy is going to be built upon, and besides aiming for inventory to stay flat or continue to decrease and continuing to repurchase stock, there is a lack of opportunities or different growth paths to enhance Dillard’s performance.

6. Dillard’s Stock Valuation and Conclusion

Although Dillard’s stock is currently trading at $339 with a P/E of 6.82 and the company has a strong balance sheet with low debt, we think Dillard’s is moving forward to a significant decrease from its current level, which will be triggered by normalization of customer demand and a return to the company’s historic profitability as no significant change or improvement occurred during the last 5 years for Dillard’s to justify the continuity of its recent growth, and we are seeing that in the contraction that Dillard’s has experienced in its sales and profit margins. Therefore, we consider Dillard’s stock to be more than 40% overvalued.

7. Disclaimer

The information in this article and on our website does not constitute financial advice, investment advice, trading advice, or an offer to buy or sell any currency, product, or financial instrument. All information found here is purely for informational and educational purposes. You should not treat any opinion expressed by Unlazy Investing as a specific inducement to make a particular investment or to follow a particular strategy, but only as an expression of opinion.